Emergencies are an inevitable part of life, often striking when least expected. Whether it’s a sudden medical expense, a car breakdown, or an unforeseen job loss, having a financial safety net can make all the difference. This is where an emergency fund comes in. An emergency fund provides financial stability and peace of mind in times of crisis, allowing you to navigate life’s uncertainties without falling into debt or jeopardizing your long-term financial goals.

What is an Emergency Fund?

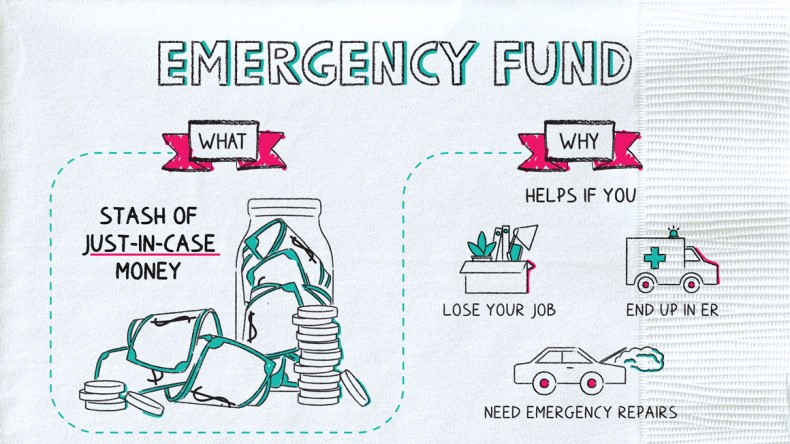

An emergency fund is a dedicated savings account reserved for unplanned expenses or financial emergencies. Unlike regular savings, these funds are not meant for discretionary spending like vacations or luxury items. Instead, they are a buffer to cover essential and unexpected costs, ensuring you can manage financial surprises without relying on credit cards, loans, or dipping into retirement savings.

Why is an Emergency Fund Important?

Financial Security and Peace of Mind

Life is unpredictable, and unexpected expenses can be a significant source of stress. An emergency fund acts as a safety net, providing you with the confidence that you can handle financial surprises without disrupting your daily life or long-term plans.

Avoiding Debt

Without an emergency fund, many people turn to credit cards, payday loans, or personal loans to cover unexpected expenses. These options often come with high interest rates, leading to a cycle of debt that can be challenging to escape. An emergency fund allows you to cover these costs without incurring additional financial burdens.

Protecting Your Investments

When faced with an emergency, you may be tempted to sell investments or withdraw from retirement accounts to cover costs. Doing so can have long-term consequences, including penalties, taxes, and lost growth potential. An emergency fund helps protect your investments and keeps your financial plan on track.

Job Security and Income Stability

In today’s volatile job market, layoffs and income interruptions are common. An emergency fund can cover essential living expenses while you search for a new job or recover from income loss, ensuring you can meet your obligations without undue financial strain.

How Much Should You Save in an Emergency Fund?

Determining the ideal size of your emergency fund depends on various factors, including your monthly expenses, income stability, and personal circumstances. Here are some guidelines to help you calculate the right amount:

General Rule of Thumb

Financial experts often recommend saving three to six months’ worth of essential living expenses in an emergency fund. Essential expenses include rent or mortgage payments, utilities, groceries, transportation, insurance, and minimum debt payments.

Assess Your Monthly Expenses

Start by calculating your monthly essential expenses. This will give you a clear picture of how much money you need to maintain your basic living standards. For example, if your monthly expenses total $3,000, you should aim to save between $9,000 and $18,000 for your emergency fund.

Consider Your Employment Situation

If you have a stable job with a consistent income, a three-month emergency fund may suffice. However, if you work in a volatile industry, are self-employed, or have irregular income, aim for six months or more to account for potential income gaps.

Account for Dependents

If you have dependents, such as children or elderly family members, your emergency fund should be larger to cover their needs. This includes childcare, healthcare, and other essential expenses.

Factor in Your Health and Insurance Coverage

If you have chronic health conditions or limited insurance coverage, you may need a larger emergency fund to cover potential medical emergencies. Evaluate your health needs and insurance policies when determining your savings goal.

Adjust for Lifestyle and Risk Tolerance

Your lifestyle and risk tolerance also play a role in determining how much you should save. If you prefer a more conservative approach, aim for the higher end of the recommended range. Conversely, if you are comfortable taking calculated risks, you might opt for a smaller fund.

Strategies to Build Your Emergency Fund

Building an emergency fund takes time and discipline, but the peace of mind it provides is well worth the effort. Here are some practical strategies to help you get started:

Set a Savings Goal

Define a specific savings target based on your monthly expenses and personal circumstances. Having a clear goal will help you stay motivated and track your progress.

Create a Budget

A budget is essential for identifying areas where you can cut back and allocate more money toward your emergency fund. Track your income and expenses to find opportunities for savings, such as reducing dining out, entertainment, or subscription costs.

Automate Your Savings

Set up automatic transfers from your checking account to a dedicated savings account. Automating your savings ensures consistency and reduces the temptation to spend the money elsewhere.

Start Small and Build Gradually

If saving three to six months’ worth of expenses feels overwhelming, start with a smaller goal, such as $500 or $1,000. Once you reach this milestone, continue building your fund incrementally.

Use Windfalls Wisely

Use windfalls like tax refunds, bonuses, or gifts to boost your emergency fund. These unexpected funds can significantly accelerate your savings progress.

Reduce Unnecessary Expenses

Evaluate your spending habits and identify non-essential expenses you can cut. Redirecting this money into your emergency fund can help you reach your goal faster.

Earn Extra Income

Consider taking on a side gig or freelance work to supplement your income. Use the additional earnings to contribute to your emergency fund.

Where to Keep Your Emergency Fund

The location of your emergency fund is just as important as its size. It should be easily accessible, safe, and separate from your everyday spending accounts. Here are some options to consider:

High-Yield Savings Account

A high-yield savings account offers a secure place to store your emergency fund while earning interest. These accounts are easily accessible and typically insured by the FDIC or NCUA, providing peace of mind.

Money Market Account

Money market accounts often provide higher interest rates than traditional savings accounts while maintaining liquidity. They are a good option for storing larger emergency funds.

Certificate of Deposit (CD) Ladder

If you have a large emergency fund, consider using a CD ladder to earn higher interest. However, ensure you have a portion of your fund in a more accessible account for immediate needs.

Avoid Risky Investments

Avoid keeping your emergency fund in stocks, mutual funds, or other high-risk investments. These assets can fluctuate in value and may not be readily available when needed.

When to Use Your Emergency Fund

An emergency fund is for genuine emergencies that are both unexpected and necessary. Here are some scenarios where using your fund is appropriate:

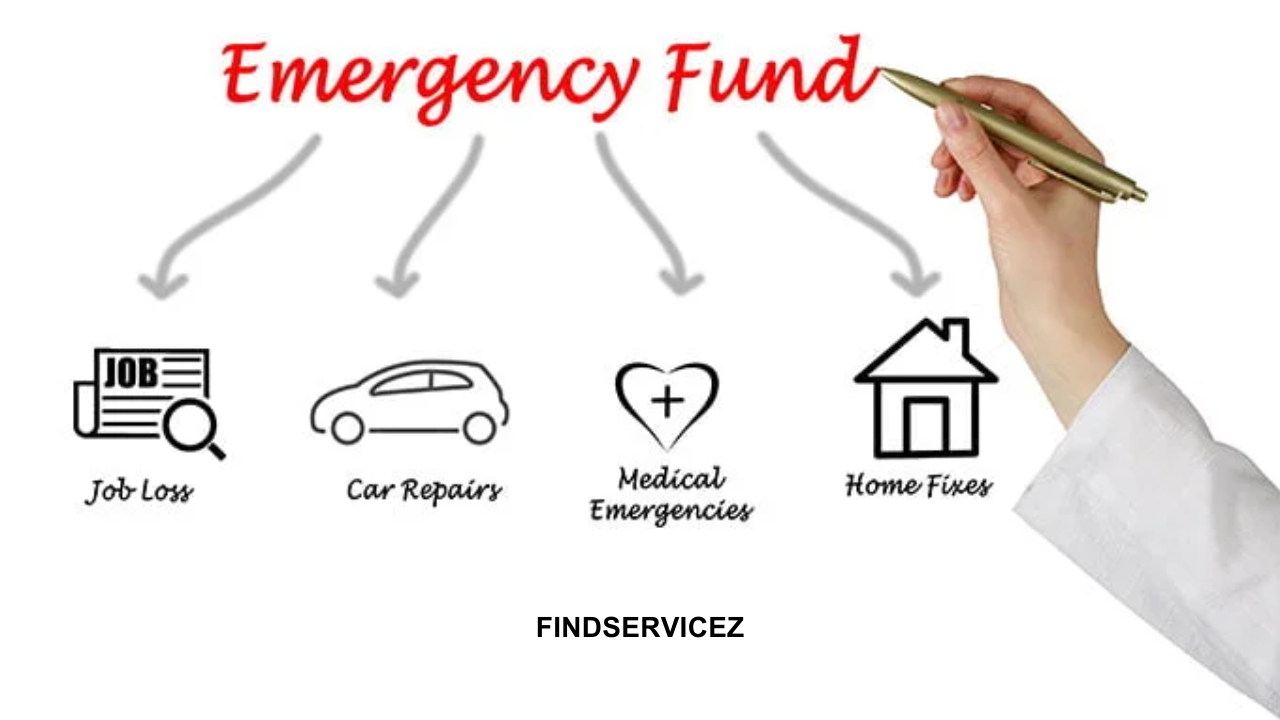

- Medical Emergencies: Covering unexpected medical bills, prescriptions, or treatment costs.

- Job Loss: Paying for essential living expenses while you search for new employment.

- Car Repairs: Addressing urgent vehicle repairs that affect your ability to commute.

- Home Repairs: Fixing critical home issues, such as plumbing or HVAC repairs.

- Unexpected Travel: Traveling for family emergencies, such as a funeral or urgent care.

Replenishing Your Emergency Fund

After using your emergency fund, make it a priority to replenish it as soon as possible. Resume saving regularly, adjust your budget if necessary, and consider temporary cost-cutting measures to restore your financial cushion.

Common Mistakes to Avoid

Building and maintaining an emergency fund requires careful planning and discipline. Avoid these common mistakes to ensure your fund serves its purpose effectively:

- Using the Fund for Non-Essential Expenses: Reserve your emergency fund for true emergencies, not discretionary spending.

- Not Saving Enough: Underestimating your needs can leave you vulnerable in a crisis. Aim for a sufficient cushion to cover unexpected expenses.

- Neglecting to Replenish the Fund: Failing to rebuild your emergency fund after use can leave you unprepared for future emergencies.

- Combining Funds with Other Savings: Keep your emergency fund separate from other savings to avoid accidental spending.

The Long-Term Benefits of an Emergency Fund

An emergency fund is more than just a short-term safety net; it’s a cornerstone of financial stability and resilience. By preparing for the unexpected, you can:

- Reduce financial stress and improve overall well-being.

- Avoid debt and maintain a healthy credit score.

- Protect your long-term financial goals and investments.

- Build confidence in your ability to handle life’s uncertainties.

An emergency fund is a critical component of any sound financial plan. It provides the security and flexibility needed to navigate unexpected challenges, ensuring you can maintain your financial stability and focus on your long-term goals. By assessing your needs, setting a realistic savings target, and consistently building your fund, you can create a financial cushion that safeguards your future and offers peace of mind. Start today, and take the first step toward a more secure and resilient financial future.